What are the eligibility criteria most likely to be of concern to emerging growth companies funded by angel or institutional investors considering funding from the Paycheck Protection Program (“PPP”)? As entrepreneurs look to weather the economic disruption caused by the COVID-19 pandemic, we address this key question and many others in this overview of one of the most significant federal bailout actions in U.S. history.

PPP is a federal program that provides up to $10 million in loans to small businesses undergoing financial strain due to COVID-19. In total, $659 billion has been authorized for PPP, with $349 billion initially authorized by the passage of the Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) on March 27, 2020. An additional $310 billion was authorized pursuant to the Paycheck Protection Program and Health Care Enhancement Act signed into law on April 24, 2020.

The United States Small Business Administration (the “SBA”), which administers the PPP, together with the U.S. Treasury, provided guidance for the PPP, primarily by issuing the April 2, 2020 Interim Final Rule, the April 3, 2020 Interim Final Rule, the April 14, 2020 Interim Final Rule and most recently, the April 24, 2020 Interim Final Rule.

Under the PPP, a company can generally borrow two and a half times their average monthly payroll costs (excluding annualized compensation in excess of $100,000 per employee) incurred 12 months before the date the loan is made. The interim final rules provide that PPP loans can be used for a variety of business purposes, and the portion of loans used for payroll costs, and mortgage interest, rent, and utility costs (if incurred pursuant to agreements in place prior to February 15, 2020), for the eight-week period following the origination of the loan are eligible for loan forgiveness, with the amount forgiven nontaxable at the Federal level (individual States may or may not follow). The loans are subject to a 1.00% fixed interest rate, 2-year term, with no collateral or personal guarantee required, and are not be subject to any prepayment penalties.

PPP loan applicants are not required to meet standard underwriting requirements (such as minimum credit score), but they must, among other things: (i) certify that “[c]urrent economic uncertainty makes [the] loan request necessary to support … ongoing operations,” (ii) certify that the funds will be used for the permitted uses, (iii) certify that they have not received duplicative PPP loans nor do they have any pending duplicative PPP loan applications (although applying for an additional loan under the Economic Injury Disaster Loan Program, in addition to a PPP loan, is not precluded), (iv) provide documentation evidencing that they have been paying their employees and their respective payroll taxes as of February 15, 2020, and (v) provide documentation evidencing that employ no more than 500 employees (although for certain industries, businesses with a greater number of employees can be if they meet applicable SBA employee-based size standards).

It’s important to note that in the April 24, 2020 Interim Final Rule, the SBA emphasized the need for borrowers to seriously consider their certification that the loan was necessary to support ongoing operations. Companies with alternative access to capital may be asked to justify their determination that the loan was in fact necessary. Borrowers who determine, after accepting funds, that they did not meet these criteria, can return funds by May 7, 2020, without penalty. Past and future borrowers must also consider the potential impending wave of criminal investigations and civil proceedings under the False Claims Act, under which the government may seek (including as a result of tips from whistle-blowers) to recover funds obtained under allegedly false or fraudulent manner.

In addition, companies considering a loan under the PPP should weigh the benefits of receiving the loan against potential negative publicity, most recently seen when it was disclosed that Shake Shack and Ruth’s Chris Steakhouse received $10.0 million and $20.0 million, respectively, under the PPP (which funds have since been returned by these companies). Anecdotally, a number of venture capitalists that have invested in our clients have advised their portfolio companies against applying for PPP loans to avoid negative public perception of “well-funded” VC startups taking the PPP funds from companies that need such funding without alternate sources of capital.

The April 24, 2020 Interim Final Rule provides instructive guidance by specifically highlighting that private equity firms or hedge funds are ineligible for PPP loans, because their businesses are “primarily engaged in investment or speculation.”

To determine the number of employees the SBA would consider to be employed by a loan applicant, the SBA’s “Affiliation Rules” apply to PPP loans (subject to a few exceptions). Generally, these rules mandate that the number of employees of a business also include the number of employees of its affiliates. Initially, based on language of the CARES Act alone, the existing, expansive affiliation tests set forth in 13 CFR § 121.103 would apply, and those include a broad “totality of the circumstances” approach. However, on its website the SBA released updated Affiliation Rules which, together with the April 3, 2020 Interim Final Rule, appear to limit the applicability of the Affiliation Rules to four tests specified in 13 CFR § 121.301(f):

(1) Affiliation Based on Ownership (Control): A PPP loan applicant is an affiliate of an individual, concern or entity that owns or has the power to control more than 50 percent of the business’s voting equity. However, a minority shareholder can also be deemed to have control, and therefore trigger affiliation, if the shareholder “has the ability, under the concern’s charter, by-laws, or shareholder’s agreement, to prevent a quorum or otherwise block action by the Board of Directors or shareholders.” As explained in more detail below, angel or institutional investors commonly possess certain negotiated rights, commonly referred to as “protective provisions,” in a company’s Certificate of Incorporation and investment agreements, such as an investor rights agreement. These rights often grant investors rights to block certain actions of the Board of Directors or shareholders of a company, and must be carefully considered to determine whether they trigger affiliation. If affiliation is triggered, the employees of the investor’s other portfolio companies, on an aggregate basis, would be included to determine whether the 500 employee size limit is exceeded.

(2) Affiliation Through Indirect Ownership: A PPP loan applicant can be deemed to be an affiliate of an individual that has the power to control based on options, convertible securities, and agreements to merge. Ownership of issued and outstanding equity securities alone is thus not a sufficient test to determine control.

(3) Affiliation Through Common Management: A PPP loan applicant can be deemed to be an affiliate of its CEO or President or other leading officers or directors that control the management of the applicant and another business. For example, if two companies share a CEO, the two businesses would be deemed affiliates.

(4) Affiliation based on Identity of Interest: Close relatives with identical or substantially identical business or economic interests are affiliates of the business applicant.

The April 24, 2020 Interim Final Rule clarified that a business with an employee stock ownership plan does not trigger the affiliation rules because participants under such plans are typically no longer employees by the time they exercise their rights to receive equity in the company.

Of the four tests, the first test of affiliation through direct ownership (control) is likely to be the most relevant to funded startups and emerging growth companies.

As it applies to majority owners, the first test is straightforward: if any shareholder, including an investor, has voting control of the company as an owner of the majority of the company’s securities, the shareholder is an affiliate of the startup. In previously issued internal guidance of the SBA concerning affiliation, the SBA provides the following example:

Company A owns Companies B, C and D (54.5%, 81%, and 60% respectively). Company A has the power to control Companies B, C and D. The companies are all affiliated.

Accordingly, affiliation through ownership can exist even where the majority owner does not play an active role in the management or operations of the business. The ability to vote the equity of the company to appoint directors would be sufficient to establish affiliation. The April 24, 2020 Interim Final Rule further emphasized that the SBA affiliation rules apply to companies held in private equity portfolios.

As it applies to the control rights of minority shareholders who have negative control rights, however, the first test requires a more nuanced analysis. Case law of the SBA’s Office of Hearings and Appeals (“OHA”) distinguishes between protective provisions that are intended to control operational and management decisions beyond those necessary to simply protect the investment made by the shareholder. These cases interpret the affiliation rules under 13 C.F.R. § 121.103 (as opposed to the 13 CFR §301(f), the applicable standard of PPP loan eligibility) but its principles can be used for guidance for PPP loan eligibility. To avoid triggering affiliation, the protective provisions held by an investor would need to be narrowly tailored to specific rights designed only to protect its investment. To the extent protective provisions grant the investor rights to more broadly control operational and management decisions of the company, whether at the shareholder or Board of Directors level, it would be more likely that such investor is an affiliate.

In today’s angel and venture deals, the Model Legal Documents of the National Venture Capital Association propose standard protective provisions often used as a baseline in negotiations between emerging companies and their investors. Using such form documents, these rights are typically documented in a company’s Certificate of Incorporation filed with the secretary of state in the company’s jurisdiction of formation, as well as in an “Investor Rights Agreement” executed by the company and its investors.

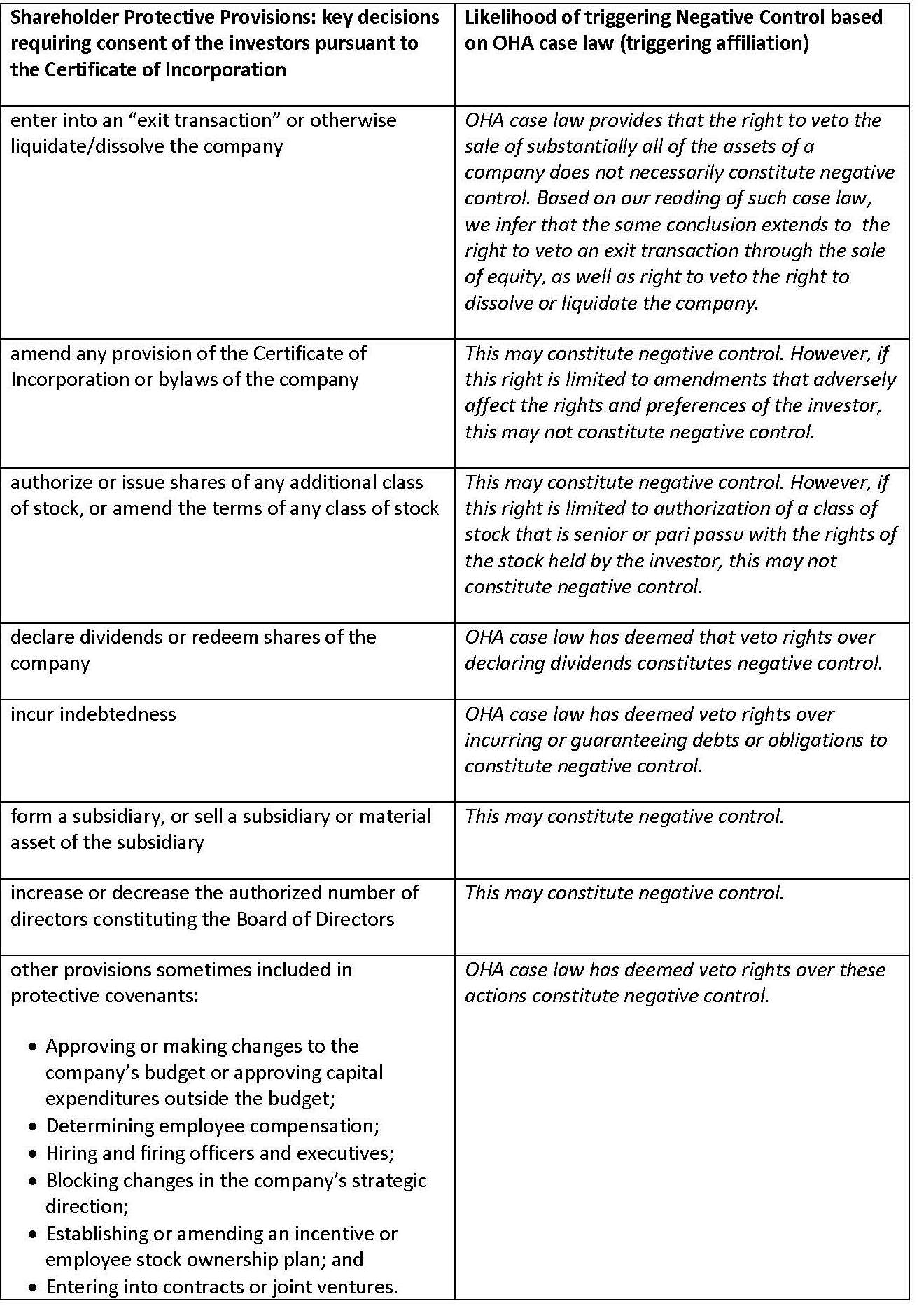

The protective provisions in the Certificate of Incorporation typically grant rights to the investors to vote, as a single class, on key decisions of the shareholders (“Shareholder Protective Provisions”). In the table below we list common Shareholder Protective Provisions and distinguish which of these, in our view, tend to trigger affiliation in accordance with OHA case law.

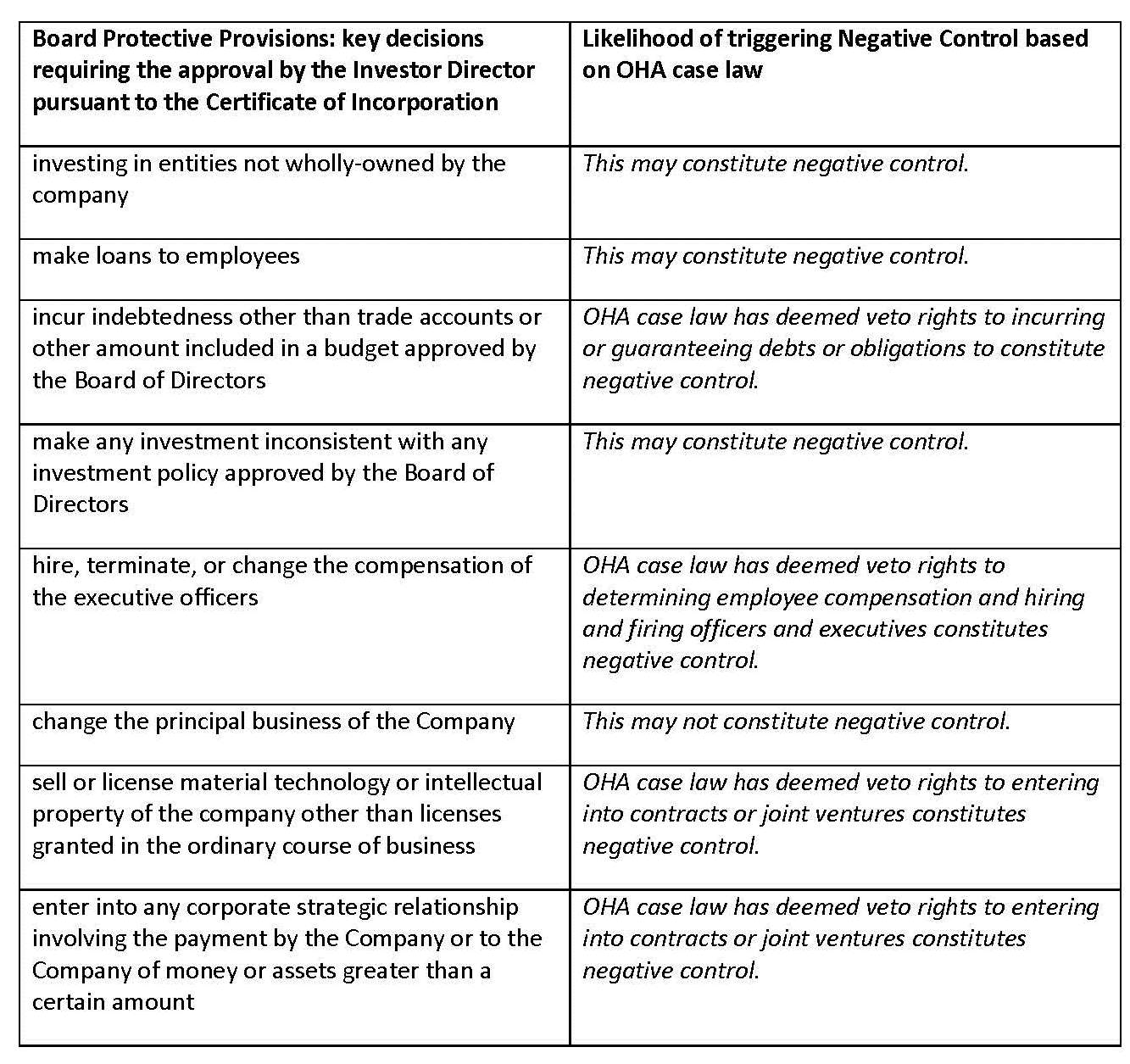

Additionally, the Certificate of Incorporation typically governs the constitution of the company’s Board of Directors, which often includes a right of the investors to appoint at least one director to the Board of Directors for each class of investors (in each case, a “Investor Director”). Conversely, the Investor Rights Agreement typically specifies certain corporate actions that require approval of the Board of Directors, with decisions subject to a veto right held by the Investor Director (“Board Protective Provisions”). In the table below we list common Board Protective and distinguish which of these tend to trigger affiliation in accordance with OHA case law.

To be clear, the standard developed by OHA case law, as articulated in a recent 2018 size appeal, to determine whether or not the protective “provisions are crafted to protect the investment of the minority shareholders, and not to impede the majority’s ability to control the concern’s operations or to conduct the concern’s business as it chooses” turns on the facts and circumstances of each case. Accordingly, a stakeholder may be able to demonstrate that its veto right with respect to operational decisions should not be deemed to constitute negative control. Conversely, in certain cases, it possible that the particular blocking rights of a stakeholder, even if such provisions would not typically constitute negative control, would nevertheless trigger affiliation given the totality of circumstances in that case. For these reasons, we did not provide conclusive determinations for each protective provision, but instead simply summarized how the OHA has ruled on such provisions in the past.

Pursuant to guidance provided by the SBA in an FAQ format (see question 6), companies and their investors may amend the relevant governing documents of the Company to revise or remove the protective provisions that trigger affiliation. As illustrated above, such amendment may not require the wholesale removal of protective provisions to avoid affiliation. Instead, a careful approach to narrowly tailor each protective provision, aligning them with an intent to protect the investment made by the shareholder and removing those intended to control operational and management decisions beyond those necessary, could be sufficient. Importantly, however, the SBA guidance indicates that any such waivers must be irrevocable. Based on this, if the parties enter into a “springing waiver” which would terminate the effectiveness of the waiver upon repayment or forgivingness of the PPP loan, the waiver would not be sufficient to avoid affiliation because it is not irrevocable. However, even if waived by investors in connection with the PPP loan, it is likely that these rights would once again be negotiated for and included in the charter and investment agreements in connection with future funding, although it is possible that rights waived by prior investors may not be offered in subsequent rounds.

Based on the information above, we recommend the following steps as angel or venture backed companies consider and apply for a PPP loan:

Please feel free to reach out to us directly should you have any questions as to whether the affiliation rules may or may not impact your ability to apply for a PPP loan, and whether or not your charter documents or investor agreements with minority investors may require an amendment or waiver.

Paul negotiates and executes buy and sell-side mergers and acquisitions. He is the co-leader of Procopio’s Mergers & Acquisitions practice. Paul also helps entrepreneurs and their investors get companies formed, funded and sold, including initial formation of corporations and LLCs, negotiation of seed, early and mid-stage equity financings. He is adept at venture capital investments, public and private securities offering and compliance and general business counseling. Paul has also counseled some of San Diego’s most successful companies in Securities and Exchange Commission compliance and general corporate governance.

Paul negotiates and executes buy and sell-side mergers and acquisitions. He is the co-leader of Procopio’s Mergers & Acquisitions practice. Paul also helps entrepreneurs and their investors get companies formed, funded and sold, including initial formation of corporations and LLCs, negotiation of seed, early and mid-stage equity financings. He is adept at venture capital investments, public and private securities offering and compliance and general business counseling. Paul has also counseled some of San Diego’s most successful companies in Securities and Exchange Commission compliance and general corporate governance.

Patrick Ross, Senior Manager of Marketing & Communications

EmailP: 619.906.5740

Suzie Jayyusi, Senior Marketing Coordinator Events Planner

EmailP: 619.525.3818

Francisco Sanchez Losada, Marketing and Client Relations Manager

EmailP: 619.515.3225

Sanae Trotter, Senior Manager for Client Relations

EmailP: 650.645.9015